Avaada Group has successfully finalized $950 million (approximately Rs 9,000 crore) in debt financing, a landmark capital procurement milestone aimed at de-risking its aggressive expansion into India’s high-value renewable segments. The multi-tranche package achieves financial closure for the nation’s largest Firm and Dispatchable Renewable Energy (FDRE) project in Bikaner and two strategic utility-scale solar ventures in Rajasthan and Gujarat. This transaction marks a sophisticated pivot in the group’s capital structure—shifting away from high-cost, dollar-denominated debentures toward a diversified blend of offshore loans and local non-convertible debentures (NCDs) to optimize its weighted average cost of capital (WACC) ahead of a planned IPO for its manufacturing arm, Avaada Electro.

Strategic Capital Structuring and Lender Consortium

The current $950 million raise is distinct from Avaada’s previous financing cycles, including the Rs 8,500 crore refinancing round in January 2025 and the Rs 4,471 crore NaBFID-led refinancing in 2024. By engaging a robust consortium of global and domestic financial institutions, the group has successfully reduced its exposure to currency volatility. The financing was raised through separate consortiums for the three utility-scale projects, involving:

- Standard Chartered Bank

- State Bank of India (SBI)

- HSBC

- DBS

- Sumitomo Mitsui Banking Corporation (SMBC)

- Mitsubishi UFJ Financial Group (MUFG)

- BNP Paribas

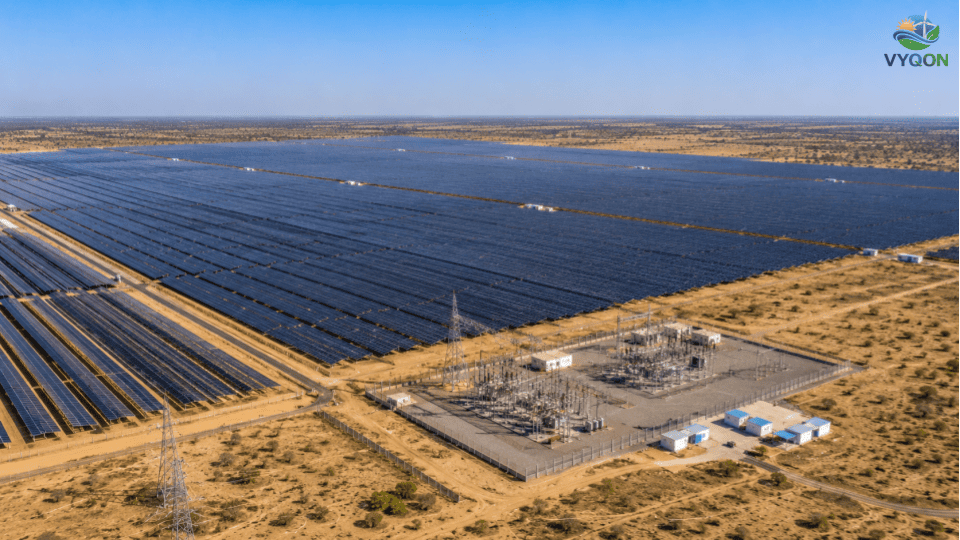

Project Breakdown and Technical Specifications

The portfolio supported by this financing represents a shift toward demand-aligned, grid-stable energy solutions. Notably, the Gujarat project details have been refined to reflect technical AC/DC splits for greater forensic precision.

| Project Type | Location | Capacity | Offtake Partner (PPA) |

| Bikaner FDRE Project | Bikaner, Rajasthan | ~1,410 MW (Total SJVN Contracts) | SJVN |

| Rajasthan Solar Project | Rajasthan | 300 MW | NTPC |

| Gujarat Solar Project | Bhachau, Kachchh district, Gujarat | 200 MW (AC) / 268.35 MW (DC) | SECI (Fixed tariff: Rs 2.61/unit) |

Technical Evolution: Scaling the FDRE Segment

The “Firm and Dispatchable Renewable Energy” (FDRE) model represents the next generation of Indian energy infrastructure. By integrating renewable generation with Battery Energy Storage Systems (BESS), the Bikaner project moves beyond traditional intermittent supply to provide “round-the-clock” power that competes directly with thermal base-load.

However, this sophistication introduces new operational rigors, specifically regarding penalties for failing to meet stringent Demand Fulfillment Ratios (DFR). Vineet Mittal, Chairman of Avaada Group, noted the significance of the closure: “This landmark financing is not just a milestone for Avaada but a defining moment for India’s renewable energy evolution. The successful closure of India’s largest FDRE financing transaction demonstrates growing confidence in advanced clean energy solutions capable of delivering reliable, round-the-clock green power at scale.”

Operational Trajectory and IPO Readiness

All three projects are currently under construction, with a commissioning window targeted for the 2027–2028 financial year. These assets are vital to Avaada Group’s broader strategic roadmap to reach 11 GW of capacity by 2026 and 30 GW by 2030.

The parent entity, Avaada Energy Private Limited (AEPL)—backed by a 39.9% stake from GPSC (part of Thailand’s PTT Group)—maintains an operating portfolio of 6.9 GWp and a total portfolio of 25.9 GWp (including 19 GWp under development). The current debt optimization is a critical precursor to the upcoming IPO of Avaada Electro, as the group seeks to fortify its balance sheet and improve free cash flow visibility.

Credit Analysis: Strengths and Strategic Exposure

Credit Strengths

- Revenue Visibility: Presence of 25-year long-term Power Purchase Agreements (PPAs) ensures stable, predictable cash flows.

- Offtake Quality: Low counterparty risk through agreements with highly-rated central entities including SECI, SJVN, and NTPC.

- Institutional Backing: Strong parentage and a proven track record in EPC execution and project development within the renewable sector.

- Asset Diversity: Geographical spread across Rajasthan and Gujarat provides significant diversification benefits.

Identified Risks and Challenges

- Leveraged Capital Structure: Interest rate sensitivity remains a concern due to floating rates and regular resets on term loans.

- Forensic Operational Risks: Potential exposure to DFR penalties and the risk of price cannibalization when liquidating surplus power in wholesale markets.

- Refinancing Requirements: The presence of five-year bullet repayments and put options necessitates a disciplined approach to future market liquidity.

- Stabilization Volatility: Under-construction assets remain susceptible to execution delays and the initial 6–12 month generation stabilization period required to reach P90 PLF levels.

Leave a Comment