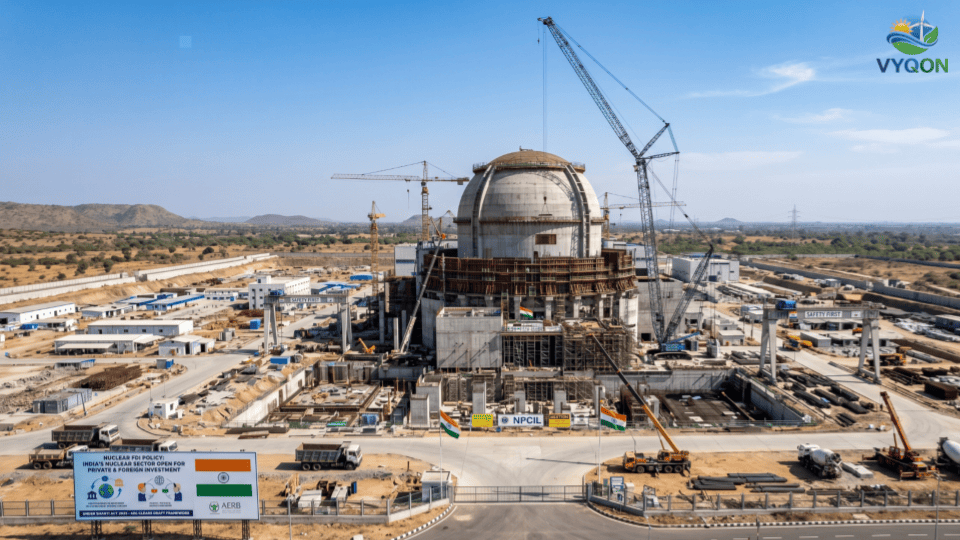

Regulatory Milestone: Bridging the ₹15 Lakh Crore Capital Gap

The Atomic Energy Commission (AEC) has formally approved a draft Foreign Direct Investment (FDI) policy framework for India’s nuclear power sector, marking a decisive shift toward dismantling the six-decade-old state monopoly. Confirmed by Seema S. Jain of the Department of Atomic Energy (DAE) during a New Delhi workshop, the draft is now entering mandated inter-ministerial consultations under the Sustainable Harnessing and Advancement of Nuclear Energy for Transforming India (SHANTI) Act, 2025.

This policy pivot is driven by stark economic necessity. To achieve the “Nuclear Energy Mission” target of 100 GW by 2047—a twelve-fold increase from the current 8.8 GW installed capacity—the sector requires an estimated investment of ₹15 lakh crore. With the Union Budget 2025-26 providing only ₹20,000 crore, the FDI framework is the primary mechanism intended to mobilize the massive capital required to bridge this funding chasm.

The New Nuclear Architecture: FDI and Statutory Oversight

The SHANTI Act, published in the official gazette on December 21, 2025, consolidated nuclear governance by repealing the Atomic Energy Act of 1962 and the Civil Liability for Nuclear Damage Act (CLNDA) 2010. The draft FDI policy operationalizes this shift with several core provisions:

- FDI and Incorporation Nuances: The policy permits up to 49% FDI through joint ventures (JVs) with Indian entities. Crucially, Clause 2(9) of the Act stipulates that foreign entities cannot operate as foreign-domiciled branches; any foreign participant must invest through a company incorporated within India to be eligible for a license.

- The Dual-Permit System: To eliminate historical promoter-regulator conflicts of interest, the Act decouples project licensing from safety oversight. A “dual-permit” structure is now mandatory: the Central Government issues the commercial license, while the Atomic Energy Regulatory Board (AERB)—now granted full statutory status—independently issues “safety authorizations.”

- Licensing Eligibility: Under Clause 3(1), the operator base is expanded beyond the Nuclear Power Corporation of India Limited (NPCIL) to include private Indian companies and JVs.

- Sovereign Reserves: The state maintains exclusive control over sensitive fuel-cycle activities, including uranium enrichment above specific thresholds, spent fuel reprocessing, and high-level waste management.

Rationalized Liability: Shifting Risk to Negotiable Commercial Contracts

The SHANTI Act fundamentally reconfigures India’s liability regime to align with the Convention on Supplementary Compensation for Nuclear Damage (CSC), removing the legal “poison pills” that previously deterred international vendors like Westinghouse and EDF.

- Graded Operator Liability: Unlike the previous flat-cap regime, liability is now tiered based on thermal power. Operator liability is capped at ₹100 crore for Small Modular Reactors (SMRs) up to 150 MW, rising to ₹3,000 crore for large-scale reactors above 3,600 MW.

- The Government Backstop: Total liability per incident is set at the rupee equivalent of 300 million Special Drawing Rights (SDR), approximately ₹3,736 crore. The Central Government, via the newly established Nuclear Liability Fund, will cover the “delta” between the operator’s graded cap and the total SDR-linked limit.

- Exclusive Channeling and Recourse: By removing the “right of recourse” against suppliers (formerly Section 17(b) of the CLNDA) and the ambiguous Section 46, the Act ensures “exclusive channeling” of claims to the operator. This shifts liability from a mandatory statutory burden to a negotiable commercial contract, allowing suppliers and operators to define risk allocation privately.

Strategic Implementation: Fleet Mode and SMR Deployment

The mission to scale from 8.8 GW to 100 GW necessitates a transition from episodic project delivery to a standardized “Fleet Mode” approach. This model involves constructing multiple reactors at single sites to streamline procurement and reduce timelines from the historical 10–15 years to a projected 5–7 years.

A central pillar of this expansion is the deployment of Bharat Small Reactors (BSRs)—indigenous SMR designs (including 55 MW and 220 MW units). These are strategically targeted for captive industrial use by heavy-industry conglomerates in sectors like steel, cement, and data centers. Market signals are already appearing; the Adani Group is reportedly exploring a 1,600 MW SMR project in Uttar Pradesh in partnership with NPCIL, illustrating the burgeoning synergy between state expertise and private capital.

Current Status and Procedural Path

While the AEC’s approval of the FDI framework is a landmark step, the policy remains a draft subject to final inter-ministerial review. The implementation phase will begin only after the formal notification of rules regarding specific investment conditions and foreign equity caps under the SHANTI Act. This ongoing evolution reflects a broader strategic intent to integrate nuclear power as a stable, low-carbon baseload essential for India’s 2070 net-zero commitments.

Leave a Comment