1. Introduction: The Infrastructure-First Pivot

India’s energy landscape is undergoing a fundamental transformation, shifting from a period of chronic deficit to a strategic, utilization-led expansion. The evolution of the national grid is no longer a mere utility upgrade; it is a macroeconomic necessity. To support a projected peak electricity demand of 459 GW by the mid-2030s, the Ministry of Power and the Central Electricity Authority (CEA) have unveiled an unprecedented roadmap: the “Transmission Plan for Integration of over 900 GW Non-Fossil Fuel Capacity by 2035-36.”

This plan marks a definitive shift toward an “infrastructure-first” model. Traditionally, transmission was reactive, lagging behind generation. The new paradigm utilizes the General Network Access (GNA) regulations to preemptively build the network required to transition from a 275 GW “green” base in 2026 to a planned 900 GW of non-fossil integration by FY2036. By doing so, India is evolving its grid from a passive synchronous system into a dynamic, automated network capable of managing the inherent variability of renewables while powering emerging green hydrogen hubs, data centers, and an electrified transport sector.

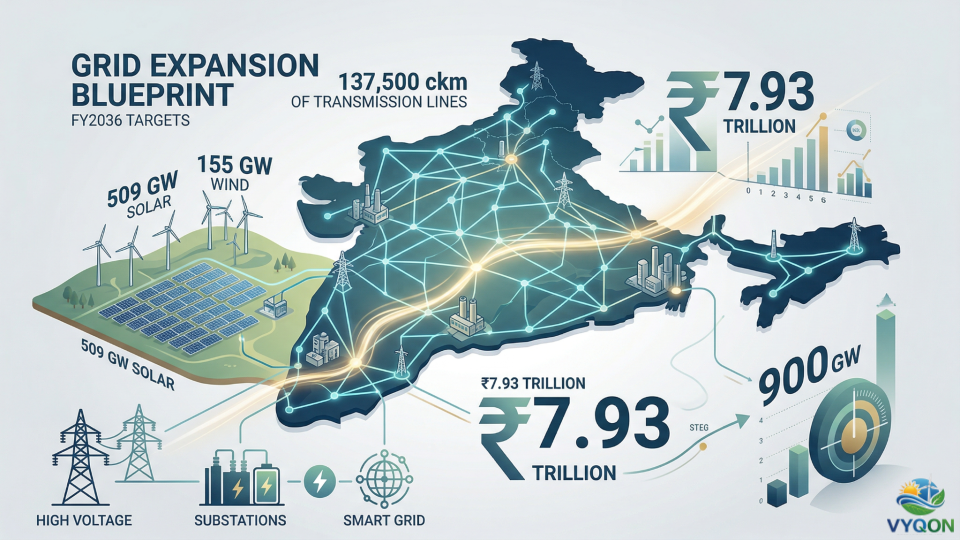

2. Quantifying the Ambition: The ₹7.93 Trillion Investment Portfolio

The financial and physical scale of this blueprint is historic. The estimated ₹7.93 trillion (approximately $84.33 billion) investment is a critical component of the $2.2 trillion total capital requirement for the Indian power sector over the next two decades.

National Grid Roadmap 2026–2036

| Metric | Projected Target (FY 2035-36) |

| Total Estimated Investment | ₹7.93 Trillion ($84.33 Billion) |

| Total Transmission Line Addition | 137,500 circuit kilometers (ckm) |

| Substation Transformation Capacity | 827,600 MVA |

| Projected Peak Demand | 459 GW |

| Annual Energy Requirement | 3,365 Billion Units (BU) |

| Total Likely Installed Generation Capacity | 1,121 GW |

| Planned Non-Fossil Integration Capacity | 913.7 GW |

The investment is split across Inter-State (ISTS) and Intra-State (InSTS) systems. While the ISTS acts as the national “power expressway,” the InSTS is vital for “last-mile” evacuation. For instance, Maharashtra alone is targeting a 35 GW local renewable evacuation capacity to support its industrial heartlands.

3. Technical Deep-Dive: Scaling Transmission for 900 GW

The roadmap is engineered to support a massive influx of renewable generation, specifically targets of 509 GW of Solar and 155 GW of Wind by 2035-36. The technical backbone relies heavily on the Green Energy Corridor (GEC) programs and strategic high-capacity links:

- GEC-III Scope: This phase represents a massive scaling effort with a ₹56,000 Crore outlay. It targets the evacuation of 134.7 GW from RE projects and 25.2 GW from pumped hydro storage. To mitigate high capital risks in complex terrains, the program includes 40% central grant assistance (₹22,400 Crore).

- Ladakh Renewable Energy Link (ISTS): Valued at ₹20,773.70 Crore, this project is a feat of engineering, involving a 5,000 MW HVDC terminal and 1,268 ckm of lines to connect high-altitude solar potential to the national grid.

- Gujarat GEC-III: A dedicated ₹29,000 crore investment to develop 3,430 ckm of 765 kV lines to tap into the state’s vast renewable resource base.

4. Bridging the Gestation Gap: Why Transmission Must Lead Generation

A core strategic pillar of this plan is addressing the “gestation mismatch.” While solar and wind projects can be commissioned in 12–18 months, high-voltage transmission corridors often require 5–8 years due to complex land acquisition and Right-of-Way (RoW) clearances.

From a strategic advisor’s perspective, the CEA has adopted “structural over-planning”—designing the grid to handle 913.7 GW, significantly above the 786 GW of non-fossil capacity actually required for the energy mix. This acts as a strategic buffer, providing “plug-and-play” connectivity for developers. By building ahead of the generation curve, the government aims to eliminate curtailment and lower the risk profile for private investors, ensuring that capital is not stranded in non-performing generation assets.

5. Regional Powerhouses: The HVDC Expressways of Rajasthan and Gujarat

The geography of India’s transition is highly concentrated. Rajasthan and Gujarat are the twin pillars of the 900 GW roadmap, requiring massive “power expressways” to transfer energy to eastern and southern industrial hubs.

Rajasthan’s Phased HVDC Development Rajasthan has identified potential for over 120 GW. To evacuate this, ten 6 GW HVDC corridors are proposed under a tiered implementation schedule:

- Tier 1 (Target 2028-29): Bikaner-V (Phase IV).

- Tier 2 (Target 2035-36): Ramgarh-II/III (12 GW), Bhadla-IV/V/VI (18 GW), Barmer-III/IV (12 GW), Jalore/Sirohi/Sanchore (6 GW).

A major milestone was achieved in January 2026 with the commissioning of the 628 ckm line from Bhadla II to Sikar II, adding 1,100 MW of capacity.

Gujarat’s Offshore Frontier Beyond land-based RE, the plan includes evacuation systems for 10 GW of offshore wind split between Gujarat and Tamil Nadu. These projects require expensive subsea transmission infrastructure and are currently being aligned with Viability Gap Funding (VGF) approvals to ensure economic feasibility.

6. Grid Resilience: UHV, BESS, and Pumped Hydro

Managing a grid with 900 GW of variable energy requires advanced voltage management and massive storage depth.

- UHV Integration: The roadmap introduces 1150 kV Ultra-High Voltage (UHV) AC systems. These are specifically designed for massive, long-distance power transfers to green hydrogen hubs in Odisha and the eastern industrial belts, minimizing transmission losses.

- The Storage Imperative: Beyond 2030, the grid requires at least 6 hours of long-duration storage for stability. The plan integrates a 100 GW Hydro Pumped Storage (PSP) roadmap and 44.8 GWh of Battery Energy Storage (BESS). Significant tenders are already moving, such as RECPDCL’s 2 GW PSP tender in Karnataka.

- Operational Optimization: By utilizing 176 GW of transmission margin available during “Non-Solar Hours,” wind and storage developers can maximize grid utilization, ensuring the ₹7.93 trillion investment produces round-the-clock value.

7. Strategic Market Opportunities: TBCB vs. RTM

The investment landscape is a competitive arena between the state-owned Power Grid Corporation of India (PGCIL) and private giants like Adani, Sterlite, Tata, and IndiGrid.

Investment Landscape (as of August 2025)

| Metric | PGCIL (PowerGrid) | Private Sector Providers |

| Projects Awarded (TBCB) | 42 | 43 |

| FY2025 Market Performance | Won 26 out of 45 projects | Competitive Pressure |

| Transformation Capacity | 189,100 MVA | High Growth Potential |

| Dominant Model | RTM & TBCB | TBCB (Tariff-Based Bidding) |

The “Grid Paradox”: There is significant institutional debate regarding market concentration. Critics suggest that PGCIL’s projects under the Regulated Tariff Mechanism (RTM)—which guarantee a 15-16% return on equity—may be cross-subsidizing their aggressive bidding in the competitive TBCB sector. To ensure lower tariffs for consumers, many advisors advocate for a 100% TBCB mandate for all future major corridors.

8. Strategic Implications for Investors & Consumers

For institutional investors, the blueprint offers three “Bedrock Advantages”:

- De-risking Connectivity: Pre-built transmission removes the primary bottleneck for RE developers, reducing the risk of ROI erosion from delayed commissioning.

- Sector Convergence: The grid is being designed around Green Hydrogen and Ammonia hubs, facilitating integrated energy value chains.

- The India Energy Stack (IES): This is the digital backbone of the transition. It involves the installation of 30 crore smart meters and Phasor Measurement Units (PMUs) for real-time monitoring, aimed at reducing AT&C losses to 12-15%.

9. Implementation Headwinds: Risks to the 2036 Vision

The vision faces a sobering reality: in FY2024-25, India added only 8,830 ckm of ISTS lines against a target of 15,253 ckm—a 42% shortfall that represents the lowest expansion in a decade.

- The Land Acquisition Ordeal: Land remains a state subject. Navigating fragmented tenancy laws and converting agricultural land for substations remains a multi-year administrative hurdle.

- The Gestation Paradox: Execution delays are already costing the industry. Companies like ACME Solar and Ampin Energy have filed petitions with the CERC following 4 GW of solar curtailment in Rajasthan due to missing transmission links.

- Supply Chain & Productivity Constraints: UHV/HVDC components (transformers, thyristor valves) face a concentrated global supply chain with long lead times. Furthermore, India’s productivity gap is stark: India requires 1,500–1,600 man-days per ckm, compared to a global average of 250–300 man-days. Modernizing construction through automation is no longer optional.

10. Conclusion: The Foundation of Net Zero 2070

The ₹7.93 trillion grid blueprint is the essential foundation for India’s 2070 Net Zero goals. By architecting a network that preempts generation, the Central Electricity Authority is attempting to de-risk the energy transition for global capital. However, the success of the 2036 vision is contingent on solving the “execution-gestation” paradox. The next decade demands unprecedented coordination between central and state utilities and private developers to ensure that land, capital, and technology align with the nation’s decarbonization timeline. Only by closing the productivity gap and streamlining land acquisition can India transform this blueprint into a resilient reality.

Leave a Comment