Introduction: The Decentralization of Haryana’s Energy Grid

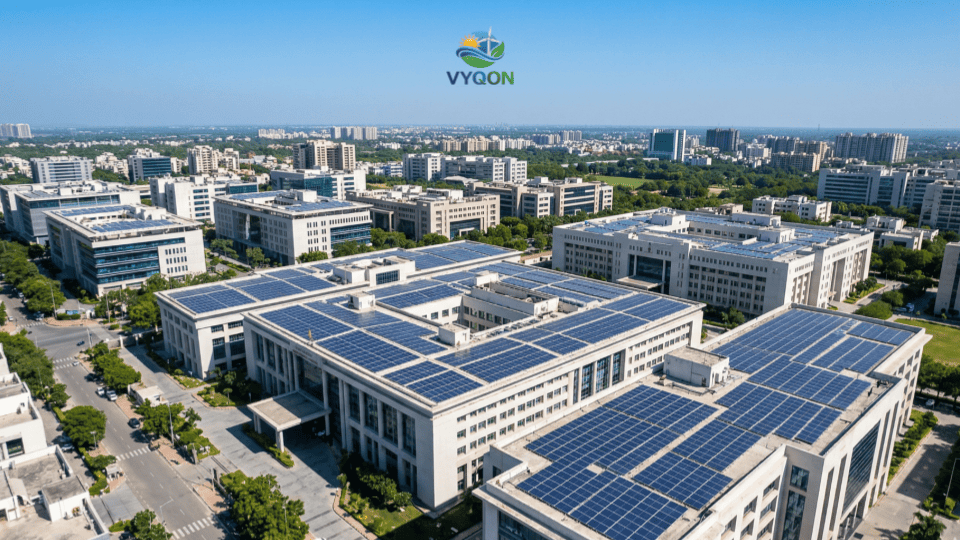

The trajectory of India’s energy transition is witnessing a profound structural pivot. While utility-scale solar parks have historically dominated the transition narrative, the focus is increasingly shifting toward decentralized, state-level infrastructure. A definitive milestone in this evolution is the recent 30.93 MW grid-connected rooftop solar tender issued by NHPC Limited for government buildings across Haryana.

This initiative, executed via NHPC Renewable Energy Limited (NHPC REL) in coordination with the Haryana Renewable Energy Development Agency (HAREDA), spans 20 districts, including economic powerhouses like Gurugram, Faridabad, and Ambala. Beyond mere capacity addition, this tender signals an institutional metamorphosis for NHPC. Originally the National Hydroelectric Power Corporation, the entity is strategically repositioning itself as a diversified renewable energy intermediary and Project Management Consultant (PMC). By leveraging its technical and financial stability to facilitate state-level energy transitions, NHPC is providing a replicable framework to help India reach its 500 GW non-fossil fuel capacity mandate by 2030.

Tender Link: https://www.nhpcindia.com/tenders

The RESCO Revolution: Shifting Risk and Capitalizing Efficiency

The Haryana tender adopts the Renewable Energy Service Company (RESCO) model, a “Service-Based Utility Paradigm” that departs from traditional government-funded capital expenditure (CAPEX). Under this framework, the Rooftop Developer (RTD) retains ownership of the asset, while the government entity—the off-taker—pays only for the energy consumed over a standardized 25-year Power Purchase Agreement (PPA).

This model effectively eliminates the upfront financial burden for government departments, transferring the entire lifecycle risk—from engineering to long-term maintenance—to the private developer. Crucially, the developer’s revenue is strictly dependent on energy output, creating a natural financial incentive to maximize system uptime and performance ratios.

Risk Allocation: RESCO Model

| Developer Responsibility | Off-taker Benefit |

| Asset Ownership: Full responsibility for Design, Engineering, and Procurement. | Zero Upfront Cost: No capital expenditure required from the government department. |

| Execution Risk: Complete responsibility for Installation and Commissioning within 9 months. | Performance-Based Revenue: Payment is strictly for energy produced; revenue ceases during downtime. |

| Lifecycle Risk: 25-year Operation & Maintenance (O&M), including component replacement. | Institutional Security: NHPC oversight ensures long-term contract adherence and technical standards. |

Rigorous Benchmarks: Financial and Technical Eligibility

NHPC has instituted rigorous eligibility criteria to ensure that only resilient, well-capitalized entities participate. These benchmarks move the rooftop sector closer to utility-scale professional standards.

Financial Eligibility and Entry Costs

- Net Worth Benchmark: Bidders must demonstrate a minimum net worth of ₹9,000 per kW of quoted capacity.

- Liquidity Mandates: Developers must meet one of three metrics: Annual Turnover of ₹4,500/kW, PBDIT of ₹900/kW, or a confirmed Line of Credit of ₹1,125/kW.

- Project Friction Points: Analysts should note significant entry costs, including a non-refundable PMC charge of ₹1,350 per kW payable to NHPC and a Performance Bank Guarantee (PBG) of ₹2,250 per kW. These figures impact the initial Internal Rate of Return (IRR) calculations for prospective developers.

Technical and Regulatory Mandates

- Domestic Content Requirement (DCR): To qualify as a Class-I supplier, the tender mandates 50% local content, strictly adhering to “Make in India” guidelines and the Ministry of New and Renewable Energy’s (MNRE) Approved List of Models and Manufacturers (ALMM).

- High-Efficiency Standards: Aligning with recent NHPC rooftop projects, there is a clear trend toward high-efficiency modules (typically 550 Wp or higher) to maximize power density on limited administrative rooftop footprints.

- Execution Timeline: Successful bidders face an aggressive 9-month commissioning window post-PPA, requiring highly synchronized supply chain management.

Strategic Analysis: 3 Key Takeaways for Investors and Developers

I. Navigating Regional Clusters and Industrial Integration

The 30.93 MW capacity is fragmented across 20 districts, necessitating a sophisticated logistical approach. The Earnest Money Deposit (EMD) requirements serve as a proxy for administrative rooftop density: Rohtak commands the highest EMD at ₹3.8 lakh, followed by Rewari and Faridabad at ₹2.74 lakh and ₹2.37 lakh, respectively. The inclusion of Bhiwadi, an industrial cluster near the NCR-Rajasthan border, highlights the tender’s intent for regional grid integration. Developers must balance the logistical overhead of dispersed sites against the high-yield potential of these concentrated industrial and administrative hubs.

II. The Professionalization of Long-Term O&M

The 25-year O&M requirement shifts the developer’s focus from simple commissioning to long-term asset health. In a RESCO model, a technical failure at a remote installation in Sirsa carries the same financial urgency as one in Gurugram. This tender will likely catalyze the growth of specialized, decentralized O&M teams capable of maintaining high Performance Ratios (PR) across diverse rooftop conditions, effectively professionalizing a historically fragmented service sector.

III. Domestic Manufacturing Tailwinds

The 50% local content mandate acts as a catalyst for the domestic solar supply chain. While this restricts the use of lower-cost international imports, it provides a stable, guaranteed market for Indian manufacturers listed under ALMM. This policy preference for “Class-I suppliers” signals a broader strategic priority: building domestic resilience over short-term capital savings in public sector procurement.

Comparative Context: Rooftop vs. Utility-Scale Strategy

The Haryana rooftop tender offers a distinct risk-reward profile compared to NHPC’s massive utility-scale ventures, such as its 1.7 GW ISTS-connected solar projects. While utility projects benefit from economies of scale and lower discovered tariffs (₹2.43–₹2.47/kWh), they are frequently delayed by 18–24 months due to land acquisition and high-voltage transmission bottlenecks.

Strategic Comparison: Project Archetypes

| Feature | Distributed Rooftop (Haryana) | Utility-Scale (ISTS) |

| Capacity | 30.93 MW (Aggregated) | 1.7 GW (Utility Park) |

| Execution Speed | 9 Months | 18–24 Months |

| Grid Interface | Low/Medium Voltage (LT/HT) | High Voltage (ISTS Substation) |

| Land Risk | Negligible (Existing Rooftops) | High (Acquisition & Litigation) |

| Scalability | High potential for “Greenshoe” expansion | Limited by substation capacity |

NHPC has a documented history of utilizing “Greenshoe” options to expand capacity at discovered rates. A successful outcome in Haryana could lead to a rapid doubling of capacity, utilizing the same bidding framework to further reduce long-term procurement costs.

Conclusion: A Blueprint for National Solarization

The NHPC-HAREDA coordination represents a critical advancement in overcoming the fragmentation of the rooftop solar market. By deploying a central PSU as the PMC, the project provides a level of institutional security and technical oversight typically reserved for utility-scale assets.

This tender is highly synergistic with the national PM Surya Ghar Muft Bijli Yojana, serving as a flagship for administrative decarbonization. As the bid deadline of April 22, 2026, approaches, the industry expects the resulting tariffs to set a new benchmark for public sector solar in North India. Ultimately, this project serves as a replicable blueprint, proving that distributed RESCO infrastructure is the most efficient vehicle for rapid, urban energy transitions.

Leave a Comment